Car owners usually get confused about the car’s IDV when going for an insurance policy purchase. IDV or the Insured Declared Value is an important element when you are buying a car insurance. Hence you need to have adequate information about it to buy the best protection for your four-wheeler.

What is IDV?

IDV is the maximum amount you get from the insurer in case of a total loss or theft. This sum is decided during the initial phases of the car insurance buying process. Usually, the IDV amount is decided according to the overall market value of the car.

For instance, if the invoice amount is Rs. 6 Lakhs, then, the below is the amount claimable as compensation if the car is stolen or damaged beyond repair:

1 – For 1st year the IDV will be 95% of this amount

2 – For every subsequent year, the IDV reduces by 10%

How it impacts premium?

The IDV value of your insurance directly impacts the premium. Higher IDV leads to a bigger premium amount, as you get more cover for your car. Similarly, a lower IDV lowers the premium payable. This is the reason why experts suggest a careful calculation of IDV by keeping the car’s age and current market value in mind.

What happens when you keep it too low?

To keep the premium amount low, many car owners try to keep IDV as low as possible. However, this won’t be advisable. Keeping the IDV too low can sometimes backfire in case of theft or total car loss.

In the worst case scenario, a low IDV can limit you from getting effective compensation for your loss. You will end up in loss even with the insurance as the compensation might not be adequate enough.

What happens when you keep it too high?

Going too high with the IDV is also a problem. The whole point of getting an insurance for your car is protecting yourself from a loss. But a very high IDV way beyond the market value will also be a loss-making proposition for you as a car insurance policyholder. Your premium amount would go way higher than what the car actually requires. Some policyholders also keep the IDV very high thinking that when they are selling the vehicle, this factor will help fetch a higher price for the used car. However, this is not true.

What should be the ideal amount?

The ideal amount of your IDV should be aligned with the current market value of your car. Try keeping the value as near to the market value of your car as possible. This way, you can keep yourself away from going too low or too high with Insured Declared Value.

Also, remember that the age of your car also decreases the required IDV. The older your car gets, the lesser IDV is should get.Calculating the correct Insured Declared Value for your car is critical. But, you need to be very clear about the scenarios before making your final decision.

To sign off, if you are thinking about increasing your car’s Insured Declared Value, evaluate the current market value first. Try to match that and you will find the perfect IDV and ideal insurance coverage for your car.

A car insurance policy is a mandatory requirement as per law. If you have a car and want to drive it on Indian roads, you should have a valid car insurance cover on your car. This mandate is prescribed by the Motor Vehicles Act, 1988. Since a car insurance policy is compulsory, you should have a complete understanding of the plan, its benefits and other features.

In India, there are two types of car insurance plans which are described below –

Third party liability cover

It is also called ‘liability only policy’ or ‘third party policy’. This is the bare minimum coverage which is mandated by the Motor Vehicles Act, 1988. The policy covers any financial liability you face in the following circumstances –

When a third party (any individual other than you and your car) dies due to an accident involving your car

When a third party suffers physical bodily injuries due to your car

When your car damages third party property

Benefits of third party cover

The premium is very low and it depends on the engine capacity of your car. It does not depend on the car’s age and remains fixed.

For any third party injury or property damage, you get coverage for up to Rs.7.5 lakh. In case of death, however, there is no limit to the coverage.

Third party can claim a compensation from your policy under ‘no fault liability’

Limitations of a third party cover

Though a third party policy has benefits, it has limitations too. These limitations are as follows –

The policy does not cover damages suffered by your car

If you suffer an accidental death or disablement you, usually, do not get any coverage. However, in some plans, there might be a personal accident cover of Rs.2 lakhs for the owner/driver of the car.

You don’t get a discount if you don’t make any claim in a policy year

Add-on coverage features are not available in a third party policy

The other type of car insurance policy is the comprehensive package policy also called package policy. The policy covers the mandatory third party liability and also damages suffered by you and your car. Coverage is provided for the following contingencies –

Death of a third party or bodily injury caused to a third party

Third party property damage due to your car

Damages caused due to man-made calamities like fire, theft, collisions, etc.

Damages faced by the car due to natural calamities like earthquakes, lightning, flood, hurricane, etc.

Damages faced when your car is in transit by air, water or road, etc.

Benefits of a comprehensive policy

A comprehensive car insurance policy has many benefits which include the following –

Coverage is given for both third party liability and damages faced you

Compensation is also paid when your car collides with a car or something other than another car

You can opt for various add-on coverage features

There is a no-claim discount in the premium if you don’t make a claim in any year

Limitations of a comprehensive policy

There are certain limitations under the plan which include the following –

Premiums are higher because of the comprehensive scope of coverage

Premiums increase further when add-ons are selected

Know why it is important to have comprehensive car insurance by watching this video

Add-ons in a car insurance plan

Add-ons are additional coverage features which are available in comprehensive car insurance policies at an additional premium. The most common and popular add-ons include the following –

Personal Accident/Personal Injury Protection (PIP)-This add-on covers death and disablements which you might suffer when involved in an accident.

Medical expenses –Under this add-on, the medical expenses incurred on an ambulance and treatments are covered if you are involved in an accident.

Vehicle replacement –Through this add-on the insurance company promises to replace your car with a new one of an equivalent value if your car is stolen or if it suffers a complete loss.

Rental reimbursement –When your car is at the workshop for repairs you might hire a rental car for your conveyance needs. This add-on covers the cost of such rental cars that you incur.

Zero depreciation –In case of damage, the claim is paid after deducting depreciation from the cost of the parts repaired or replaced. With this add-on, the complete cost of replacement is paid by the insurance company irrespective of the applicable depreciation.

NCB protect –When you don’t make a claim you earn a no claim discount. However, this discount is lost whenever a claim is made. This add-on ensures that even after you make a claim you don’t lose your accumulated discount.

Engine protect-This add-on covers the cost incurred in replacing or repairing the engine of your car.

Roadside assistance –This add-on ensures round-the-clock assistance by the insurer if your car breaks down. The company provides you with on-site repair and rescue services with this add-on.

Insurance being a technical concept involves the usage of a lot of jargons which are not easily understood by an average customer. So, here are some common terminologies used in your car insurance plan which you should know about –

Premium –Premium is the cost of the insurance cover you take on your car. It is required to be paid to keep your policy active.

Third party liability -Financial liability which you face when a third party suffers death or bodily injury is called third party liability. You also face this liability when you damage third party property.

Own damage premium-The premium you pay for covering the damages suffered by your car is called own damage premium. The damage suffered by your car should be through external violent means which are not in your control.

Liability coverage –The coverage you get for any third party liability is called liability coverage

Rider –It is an add-on to your insurance policy which provides additional coverage benefits. An additional premium is required to be paid and choosing a rider is optional.

Personal accident rider –This is an add-on benefit which pays a lump sum benefit if you suffer from accidental death or disablement.

No Claim Bonus (NCB)-This is a discount given on the renewal premium if you do not make any claim in the current policy year.

At fault-At fault represents the extent of your contribution to a car collision.

Insured Declared Value –This is the market value of your car after being adjusted for depreciation based on your car’s age. IDV represents the maximum claim which you can get in your car insurance policy if your car is stolen or in case of total loss.

Claim adjuster –A claim adjuster is a person who investigates and settles your claim

Zero depreciation rider-This is an add-on cover which waives off the applicable depreciation on your car’s parts and gives you a higher claim settlement

Exclusions –These are conditions and instances which are not covered in your car insurance policy.

Did you know you can reduce your car insurance premiums through various types of discounts?

Yes, car insurance providers offer a range of discounts on your car insurance premium. Here are the different discounts which you can avail to minimize your car insurance premium outgo.

Vintage car discount-If you are an owner of a vintage car you have reason to rejoice. You are entitled to a 25% premium discount on the car insurance policy for your vintage car. Vintage and Classic Car Club of India certifies cars manufactured before 31st December 1940 as vintage. So, if you have this certificate, you can claim this discount.

Membership discount –The Motor Vehicles Act, 1988 recognizes various automobile associations in India. If you drive safely you can become a member of any one of these recognized association. This membership is recommended as you can get a 5% premium discount because of your membership. The recognized associations include Automobile Association of India (AAI), Western India Automobile Association (WIAA) and Automobile Association of Eastern India (AAEI).

Anti-theft device discount-If you are a careful owner and install safety devices in your car you can get a 5% discount in your car insurance premiums. The safety devices include central lock, airbags, anti-theft mechanisms, ABS, etc. which should be approved by the Automobile Research Association of India (ARAI). Read more about Some common safety features in your car

Discount for the differently abled -If you are a handicap and have modified your car to suit your mobility needs, you can get a 50% premium discount. Moreover, institutions which are engaged specifically in serving the handicapped are also allowed this discount on their vehicles.

No Claim Bonus –In any policy year if you don’t make a claim, you earn a No Claim Bonus which gives a discount in your renewal premium. The discount starts at 20% and increases every subsequent year when no claim is made. The maximum discount that you can avail is 50%. So, avoid making small claims in your policy and protect your accumulated NCB discount. Furthermore, buy a NCB protect rider to protect your discount even in case of a claim.

Voluntary deductible discount –If you choose to pay a portion of the claim from your pockets you are choosing a voluntary deductible. Since you are lowering the burden of claim for the insurer you get a discount of 15% to 35% in your car insurance premium. So, if you are a careful driver or have a vintage car go for voluntary deductibles and lower your premiums.

The final word!

A car insurance policy is a mandatory cover. Know all about it before you actually set out to buy a policy for your car. You would be able to understand the coverage features, choose required add-ons, understand the technical parts of the plan and also enjoy attractive premium discounts.

Don’t you love having a bike? Most probably your answer would be a big ‘Yes’. Two wheelers are very popular in India because they have two major benefits. One, they are economical. Two, they are fast and a convenient mode of transport. That is why, two wheeler sales are booming. See for yourself:

Everything you should know about Two Wheeler Insurance Policies in India

Did you know that a two wheeler insurance policy is also required with your two-wheeler?

According to The Motor Vehicle’s Act, every vehicle which is running on India roads must have a valid insurance policy on it. Therefore, if you have a two-wheeler you are mandated to have an insurance policy on it too.

Insurance, being a technical concept, escapes the knowledge of many individuals. If you are also clueless about your bike’s insurance policy, here is everything which you need to know. Let’s roll –

Types of policies available

Two-wheeler insurance policies come in two different variants and each variant has different coverage features. They are –

Third party liability only policy

A third party liability only policy is mandated by law. This policy covers you against any financial liability which you might incur if you cause bodily injury, death or property damage to a third party or property through your bike. The third party can be any individual or property apart from you and your bike.

Comprehensive package policy

Where the third party cover ignores damages suffered by you and your bike, a comprehensive package policy comes into the picture. The policy has two coverage areas. One, it covers the mandatory third party liability for any damages inflicted on a third party or property. Two, it also covers any damages suffered by your bike and you. If your bike is stolen or is damaged by any man-made or natural calamity, the policy pays for the repairs. Moreover, there is also a personal accident cover for the owner/driver of the bike which pays a benefit in case of accidental death.

Add-ons available

Comprehensive two wheeler insurance policies also have various additional optional coverage features. These are called add-ons and they widen the scope of cover. Some popular add-ons include the following:

Zero depreciation cover

In case of a claim where the bike’s parts are replaced, the insurance company pays the depreciated cost of the parts. The rest is payable by you. A zero depreciation add-on is useful as it nullifies the effect of depreciation. If the cover is selected, the company pays the full cost of the part repaired or replaced irrespective of depreciation.

NCB protect

Every year when you do not raise a claim in your insurance policy, you earn a premium discount called the No Claim Bonus. This discount is applied on the renewal premium and goes as high as 50%. However, in any year if you make a claim you lose the accumulated discount. If you have NCB protect add-on, this discount is not lost even in case of a claim.

Passenger cover

There is a personal accident cover in the policy only for the owner/driver of the vehicle. If you want a cover for the pillion passenger you can opt for this add-on. It would pay a benefit in case of accidental death or disability faced by the pillion rider.

Discounts in the policy

This would sound good to you that a bike insurance policy offers various discounts on the premium. You can avail a discount for –

Buying the policy online

Installing safety devices

Using the NCB accumulated

Buying a long-term policy

How to make a claim

The last thing which is also the most important one is to understand how to make a claim on your two-wheeler insurance plan. Many of you don’t know the claim settlement process.

Here are some simple and common steps –

Inform the insurance company immediately in case of an accident if are looking to make a claim.

Take your bike to the nearest preferred garage (garage tied-up with the insurer) for cashless claim settlement. In case of non-networked garages, you would have to pay for the repairs and get it reimbursed by the company

In case of theft of the bike or for a third party claim, file an FIR

A survey is required before the bike is repaired. This survey is done by the company’s appointed surveyor. When you inform the company of the accident the company arranges for the surveyor’s visit. Only after the survey is done do the repairs begin.

After repairs, the company settles the bill and you can take delivery of your bike.

In case of theft or total loss (when the bike is beyond repairs), the company pays the IDV as a claim.

A two-wheeler insurance policy is mandatory and you should know all about the plan before you buy one. So, go through the above-mentioned pointers and understand the concept of two wheeler insurance.

Life Insurance and Health Insurance are the two major requirements in everyone’s life. Both provide financial security against unavoidable contingencies. While life insurance provides security in event of death, a health insurance policy secures your finances in a medical emergency. Since both death and illness are unavoidable contingencies, a life and a health insurance plan should feature prominently in your financial portfolio.

Yet not convinced? Here are the major reasons why life and health insurance policies are a must:

Top #3 Reasons to buy Life Insurance

Financial security

A life insurance plan pays your family a lump sum amount in the event of your death. This corpus helps in securing your family’s financial obligations even when you, the breadwinner, are not around and thus provides financial security.

Fulfilment of life’s financial goals

All of us have several life goals. We want to secure our family’s financial future in case of an emergency, secure our child’s future, build our assets and plan for our retirement. Life insurance plans, besides fulfilling the primary need of creating an emergency fund, also help in fulfilling our other life goals. We can secure our child’s future through a child plan, create assets through savings and unit-linked insurance plans and also build a retirement fund through pension plans. Thus, life insurance provides us an all-around solution for planning our life’s financial goals.

Tax saving

Yes, this is another reason which might prompt you to buy a life insurance policy. The premiums paid for your life insurance plan are exempt up to Rs.1.5 lakhs under Section 80C of the Income Tax Act. Moreover, the benefits you receive from your life insurance policy, whether on death or on plan maturity, are also tax-free. Isn’t it great?

Medical expenses are becoming very expensive. As an average middle-class individual, it becomes difficult for us to handle these high expenses. A health insurance policy pays our medical bills and thus helps us in combating large medical expenses.

Safeguarding our finances

In case of any medical emergency when the hospital bills rack up to huge amounts, we turn to our savings to pay them. High medical expenses put a strain on our savings and threaten to wipe them out. Having a health insurance plan helps us safeguard our savings from such medical expenses as the health policy itself pays for such expenses.

Tax saving

Like life insurance premiums, health insurance premiums are too exempted from tax under Section 80D. The maximum exemption you can claim is as high as Rs.60, 000 annually if you are a senior citizen and also cover your senior citizen parents under a health insurance plan.

Now we know that both life insurance and health insurance are important. But, do we know when should these plans be bought? Though both life and health insurance plans should be bought at the earliest, here’s a look at their applicability at different stages of our life.

This is the age when we set our life goals and experiment new things in life. As we are young, we tend to avoid insurance. But an early start can be of more significant value. We should have a term insurance plan for creating a contingency fund and also invest in a basic health insurance policy.

For instance, Manisha, 25, working in a leading Finance company is a young individual with limited responsibilities. Given her limited income, she should first opt for a term insurance plan. This is because a term insurance is the cheapest amongst the life insurance plans and also the premium would be lowest if purchased early.

Then, she should buy a health plan with a smaller cover which would be affordable and also sufficient if her employer already covers her in a group health plan. She should look for a health coverage with Maternity Benefit so that the basic waiting period is over well before she plans a family!

In your 30’s

At this age you not only have responsibilities of your parents but also of your wife and kids. While earlier a term plan was enough, a child plan comes into the picture in your 30s if you have kids and want to secure their future. In case of health insurance, you should increase the coverage amount as more members would be covered in your family floater plan.

As said in previous case, Manisha, when she is in her 30’s should add a child plan to her term plan. Moreover, if the coverage under term plan is not sufficient, she should increase the same.

In case of health insurance, she should opt for a Family Floater plan covering herself, spouse and her children. It will be beneficial for her as well for her family. She can also convert her existing health plan to a family floater one and either increase the coverage or opt for a Top-Up Plan for additional health coverage.

In your 40’s

At this age you should focus on creating assets. A term plan is a must and should be continued (if bought before) or bought anew. You may also opt for an endowment plan for creating sufficient savings. Retirement planning should also start from early 40s and so, a pension plan is also advised.

In case of health insurance, your Family Floater Plan is good enough but you can increase the coverage amount by a top-up health plan due to rising medical expenses and inflation. Furthermore, you can take an add-on cover for Critical illness as to protect against the rising probability of such illnesses.

So, Manisha in her 40’s can choose to buy an endowment Plan for wealth creation along with insurance protection, buy a pension plan for her retirement as well as choose a Critical Illness Plan.

In Your 50’s

Now, the time has come to think about your spouse and your future after retirement. In your 50’s, you must have a pension plan to ensure that you receive monthly income after your retirement.

Also, you should still continue your existing comprehensive health insurance plan that covers any medical emergency.

So, Manisha can proactively continue her insurance plans and if she had not opted for a pension plan earlier, it is high time to buy the same.

In Your 60’s

At this age, it is usually difficult to buy a new insurance policy, as your income would soon dry up. However, you should still consider buying a term insurance or continue your existing term plan cover for uncertain death.

In case of health insurance, you can opt for senior citizen health insurance plan. If you already have a health insurance plan, renew it religiously for comprehensive health coverage.

So, Manisha in her 60’s should continue her existing health and life insurance plans lifelong. If she finds her health coverage is inadequate or not purchased earlier, she can opt for Senior Citizen health plans with pre-existing ailment coverage as well.

They have unparalleled benefits and demand a place on our portfolio. Though buying young is ideal, life insurance and health insurance plans are also governed by your life stage. So, understand which life stage you are in and then buy the plans.

Health insurance plans have become a way of life. The rising incidence of diseases and the high cost of treating them spell doom for a common man’s finances in the absence of a health insurance plan. As such, people are becoming increasingly aware of the necessity of having valid health insurance coverage. In fact, besides covering themselves, people are also including their family members under the scope of family floater health insurance plans.

Health insurance plans are, usually, one-year plans which need regular renewals. However, nowadays, many plans allow a continuous coverage for 2 or 3 years if you pay the aggregate premium at one go. Even in these long-term plans, renewals are necessary after the term expires if you want to enjoy continuous lifelong coverage. During renewals, there are some things which you should keep in mind if you want to enjoy the best insurance experience. Do you know what these things are? Let’s find out:

The Sum Insured

We always act like a miser when buying a health insurance plan. Since choosing a higher Sum Insured proves to be expensive, we go for lower coverage levels to save premium outgoes. However, having a considerable Sum Insured is necessary if you are to face the high treatment costs. So, if you have chosen a lower Sum Insured earlier, at the time of renewal you should try and enhance your Sum Insured limit. Enhancement of your Sum Insured might also be required if new members are added to the scope of coverage. So, at the time of renewal you should analyze the sufficiency of your plan’s Sum Insured level. If low, try and increase the level and if the Sum Insured is unnecessarily high (which is rarely the case) reduce it to its optimal level and save premiums.

Every health insurance plan has some common coverage features and some unique coverage features. These unique features give the plan an edge over other plans. When you are renewing the cover, check if the existing coverage features are sufficient for your need or not. For instance, maternity coverage under your existing plan might no longer be needed if you already have utilized it. On the other hand, you might need maternity coverage if you are newly married and your existing health plan doesn’t have it.

The new members to be added

Addition of new members to an existing plan happens either after you get married or you have a child. In both these instances you are required to pay an additional premium for inclusion of additional members. So, when renewing, you should check if there are any new members who are to be added to your plan.

Premium amount

You should also consider the renewal premium amount which is being asked by your existing insurer. The premium should be compared with the coverage features to assess whether it is reasonable or not. You can also compare other health insurance plans to find lower premium quotes for similar coverage features.

Renewal of your health insurance plan should be done with careful consideration. You should take care to ensure that the Sum Insured level of your plan is sufficient for your requirements, all your family members are covered, the coverage features you need are present in the plan and the premium you are paying is reasonable. If you have any doubt there is always an option of portability. Do you know what portability is?

Health insurance portability

Portability of a health insurance policy means the facility of switching your existing health insurance plan to another plan while retaining the benefits of the existing plan. Porting can be done across different plans of the same company or another plan of another company. The No Claim Bonus you have earned in your existing policy and the waiting period which has elapsed is credited to the new policy to which you port.

Porting gives you the flexibility of switching between health plans if your requirements change or if you find a better deal. Porting is possible only at the time of policy renewal and so you should be careful. Check for the above-mentioned things on renewal and, if required, port to another plan which fulfills your requirements.

We don’t hesitate today to buy any product online, be it apparels or electronics. Do you know that now you can buy insurance online too? Our Turtle explains the various advantages of buying insurance online.

Visit Turtlemint to find the term life insurance plan that provides the best value for your money.

If you own a car in India, you would have to get your car covered under a car insurance policy. This rule has been made mandatory as per the Motor Vehicles Act, 1988. As per the Act, every vehicle, including a car, should have a valid insurance cover on it. If not, you, the owner would be held responsible for violating traffic rules and face heavy penalties.

Given the necessity of a valid insurance cover, there are different types of car insurance policies available in the market. Let’s understand what these policies are –

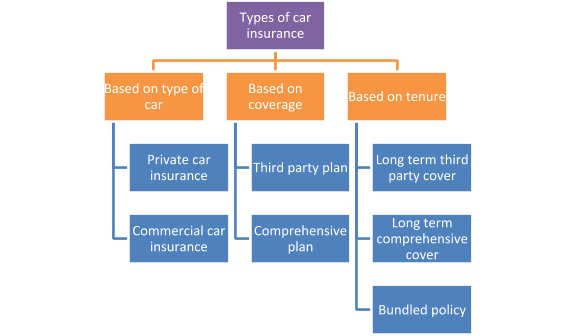

Types of car insurance based on the type of car

There are two types of car insurance policies based on the type of car that is being insured – private car insurance policy or commercial vehicle policy. Private car insurance plan covers privately owned four-wheelers while commercial car insurance plans cover taxis and other commercially used cars.

Types of car insurance based on coverage

This is, perhaps, the most common and popular basis on which car insurance policies are differentiated. Based on the coverage offered, there are two types of car insurance plans –

Third-party liability only plans

Comprehensive plans

Let’s understand these plans in details –

Third-party car insurance plans

Third-party policies cover the legal and financial liability that you face when you hurt or damage another individual due to your car. The policy covers the following types of claims –

Financial liability faced when an individual gets killed due to your car

Financial liability faced when an individual gets hurt by your car

Financial liability faced when you damage an individual’s property

Third-party plans are mandated by the Motor Vehicles Act, 1988. If you have third party coverage on your car, you are fulfilling the required rule of the Act.

Comprehensive car insurance plans

While third party plans are legally compulsory, comprehensive car insurance plans are voluntary in nature. You can choose to buy the policy for wider coverage of your car. Comprehensive car insurance plans are recommended because they also cover the damages suffered by your car besides the third party liability that you face. Thus, in comprehensive plans, you get coverage for the following contingencies –

Financial liability faced when an individual gets killed due to your car

Financial liability faced when an individual gets hurt by your car

Financial liability faced when you damage an individual’s property

Financial loss suffered when the car is damaged by natural causes like lightning, earthquake, floods, storms, cyclones, landslides, etc.

Financial loss suffered when the car is damaged by man-made causes like explosion, implosion, fire, malicious activities, riots, etc.

Financial loss suffered when the car is stolen

Financial loss suffered when the car is damaged while being transported

Comprehensive car insurance plans, therefore, have a wider scope of coverage and cover third party liability as well as damages suffered by the car.

There is also a mandatory personal accident cover which is available in both third-party and comprehensive car insurance policies. This cover is available for INR 15 lakhs and covers accidental death and permanent disability suffered due to an accident.

Types of car insurance plans based on coverage duration

As per a rule passed by the Insurance Regulatory and Development Authority of India (IRDAI), if you buy a car on or after 1st September 2018, you would have to buy a long-term car insurance plan on it. The rule mandates a long-term third party cover for three years and so, based on the rule, the following types of car insurance plans are available in the market –

Long term liability-only policy

This policy covers only third party liabilities for a continuous period of three years. The policy is available only for new cars.

Annual comprehensive policy

This policy provides third party coverage as well as coverage for the damages suffered by the car itself. The comprehensive policy, as the name suggests, is offered for one year.

Bundled policy

Since a long-term comprehensive cover might prove unaffordable for car owners, a bundled policy is also issued. Under the bundled policy, third party liability cover is allowed for three years while the comprehensive cover is allowed for one year.

For cars bought before 1st September 2018, one-year third party or comprehensive cover is valid.

Thus, car insurance policies can be differentiated on the following types –

Customizing your car insurance policy through add-ons

Comprehensive policies offer different types of car insurance add-ons. You can add these add-ons to increase the coverage benefits of your policy. Some of the most common and popular add-ons include the following –

Roadside assistance

Under this add-on, you get the promise of round the clock assistance from the insurance company for any car breakdowns that you face

Zero depreciation

This add-on enhances the claim payable under the policy by removing the deduction for depreciation on the parts of the car which have been repaired or replaced

No Claim protect

This add-on protects the accumulated no claim bonus under your car insurance policy even after you make a claim

Engine protect

The add-on covers engine damages which happen due to water seepage into the engine

Return to invoice

The add-on pays the invoice value of the car in case of theft

Medical expenses

In case of an accident involving your car if you are hospitalised and incur medical expenses, the expenses would be covered under the add-on

Roadside assistance in car insurance plans

Roadside assistance is an optional add-on that promises to offer 24*7 assistance and support if your car breaks down or stops in the middle of a remote place and you cannot find any help. The roadside assistance cover gives assistance for flat tyres, key replacement, accommodation, taxi services, fuel supply, battery jumpstart, etc.

Though the roadside assistance coverage is offered as an optional add-on with an additional premium, some plans incorporate the benefit in their coverage structure itself. You would, thus, find the roadside assistance cover inbuilt under the scope of some car insurance plans.

If you frequently take your car for long commutes or travel remotely, opting for the roadside assistance cover would be a wise choice.

How to choose the best car insurance?

When buying an insurance policy for the car, you should choose the best policy so that you get the most inclusive scope of coverage. To choose the best car insurance plan, here are some tips –

Opt for a comprehensive plan

A comprehensive plan not only covers the legal liability but also the damages suffered by your own car. Moreover, in the case of theft of the car, a comprehensive car insurance plan gives you a lump sum benefit that might help you replace the stolen car. Thus, opt for comprehensive coverage to avail of the best protection.

Choose an optimal IDV

The Insured Declared Value (IDV) is the coverage amount of the comprehensive car insurance plan. It is calculated by deducting the depreciation of the car from its market value. Insurers allow you to customize the IDV for maximum coverage. Choose an IDV as close to the value of the car as possible so that you get a high claim amount in the case of total loss or theft.

Opt for add-ons

Add-ons enhance the scope of coverage and also the claim amount. Choose suitable add-ons depending on your coverage needs to make your policy all-inclusive.

Hunt for discounts

Different types of premium discounts are available under car insurance plans. Hunt for the maximum possible discounts to reduce the premium outgo.

Opt for a wide network of garages

Networked garages allow you cashless claim benefits. So, when buying car insurance, you should opt for an insurer that has the widest network of cashless garages. This would help you locate the nearest garage easily and avail of cashless claims.

Check the CSR

The Claim Settlement Ratio (CSR) of the insurance company shows its claim settlement history. The higher the ratio, the more trustworthy the insurer. So, choose an insurer with a high CSR for a favourable claim experience.

Compare and buy

More than a dozen general insurance companies offer different types of car insurance plans. So, when buying a policy, the comparison is a must. When you compare you can find a plan that offers all the above-mentioned benefits and also costs the most reasonable.

How to buy car insurance plans?

You can buy any type of car insurance policy online or offline. For the offline mode, you can visit the insurer’s office or contact an insurance agent. For the online mode, which is much easier, you can visit the insurer’s website and buy the plan in an instant. For finding the best car insurance policy, though, you should visit platforms that allow you the facility of comparison.

Turtlemint is one such platform that allows you to compare and then find the best car insurance policy. Turtlemint is tied up with some of the best car insurance providers so that you can find only the best plans that are available in the market. To buy a suitable type of car insurance plan from Turtlemint, here are some common steps that you should follow –

Provide the details of your car like the registration number or location, make, model and variant, registration and manufacturing year, details of previous policy (if any), type of policy needed, etc.

Also provide your contact details so that you can avail of personalized services to buy the best car insurance plan

When you submit the details you would be shown a list of the best car insurance plans available in the market

Compare the different plans based on their coverage and premium

Choose the most suitable policy, fill up an online application form, pay the premium through any digital mode and your policy would be issued instantly.

Buying car insurance through Turtlemint is simple and takes only a few minutes of your time.

Making a claim under different types of car insurance plans

Claims under car insurance policies depend on the coverage offered by the policies. Thus, it is important to know the process of making a claim under each type of plan. So, here’s a brief look into the claim process of the third party and comprehensive plans –

Claim under third party policies

In the case of third party policies, the claim is reported to the Motor Accidents Tribunal where the financial liability is decided. The process is as follows –

Inform the insurance company as soon as the claim occurs

File a police FIR and the claim would be taken to the tribunal

The tribunal rules out the liability that you face and the insurance company pays the liability to the third party

Claim under comprehensive policies

Under comprehensive policies, third party claims are made as per the above-mentioned process. However, if your car suffers damage, the claim process is as follows –

Inform the insurance company immediately. The company then tells you the location of the nearest garage where you can claim cashless repair services

Take your car to the networked garage of the company where a surveyor would assess the damage and prepare a claim report

Based on the surveyor’s report the insurance company approves the claim. Once the claim is approved, repairs on your car begin

After the repairs are done the insurance company settles the bill directly with the garage. You might have to pay a part of your claim after which you can take delivery of your car

In case you get the repairs done at a non-networked garage, you have to bear the repair costs and then get the costs reimbursed by the insurer

Amidst the different types of car insurance plans available in the market, choose the policy which suits your coverage needs. A comprehensive cover is recommended as it pays for the repair costs of your car. You can also increase the coverage with available add-ons and enjoy a wider insurance cover. Since car insurance is mandatory, choose the best plan and avoid legal hassles.

Frequently Asked Questions

Do add-ons require additional premiums?

Yes, since add-ons provide additional coverage, they require additional premiums. For each add-on that you choose you would have to pay an additional premium.

Will there be premium discounts if I buy three-year comprehensive coverage?

Yes, various types of premium discounts are allowed under comprehensive car insurance plans. You can claim a discount for the following –

Long term coverage

Installing safety devices

Becoming a member of automobiles associations

Modifying the car for disabled users

Choosing voluntary deductible

Existing no claim bonus

What is the premium for personal accident cover?

A personal accident cover for INR 15 lakhs costs INR 750

If I don’t buy comprehensive plan would I face a penalty?

No, if you have bought only a third party liability policy, you would not suffer any penalty for not buying a comprehensive plan. However, if your car faces any damage, you would incur huge repair costs in the absence of a comprehensive car insurance policy.

You have a car insurance plan because it’s mandatory. But do you know all the terms written in it, to know if it’s the right one for you? Our Turtle explains these terms so you make the right choice.

A high insurance premium on car insurance may put you off. Not if you know how to bring down the premium with these discounts. Here are some discounts on car insurance plans you did not know of.

Principal Officer: Vilas Gandre,1800-266-0101+91-9833248023

Secured by:

Insurance is the subject matter of the solicitation. For more details on policy terms, conditions, exclusions, limitations, please refer/read policy brochure carefully before concluding sale.